Welcome to the fifth blog post of: Podcast of the Week. Thanks for taking an interest! If you have not yet: please check out the other Podcast of the Week blog posts: link. This blog post is about Early Retirement Extreme (ERE), which you could call the philosophy behind the FIRE movement. We will learn more about the philosophy and its underlying principles. The podcast episode is an interview with the founder of ERE, Jacob Lund Fisker.

Mad Fientist

The podcast is by Mad Fientist, Brandon Ganch. He started a blog about financial independence in early 2012. Firstly to develop strategies to retire early and secondly to find out what to do after retirement. As part of the second goal he launched the podcast, interviewing early retirees to get their perspective. In 2016 at age 34, Brandon reached financial independence. This allowed him to focus on music production, recently he launched his first album. I have been listening to the Mad Fientist for over a year now, occasionally visiting his blog. My favourite thing about his content is the variety, from funny experiments to financial goal setting. There is always something unique to find.

Why do I recommend this podcast episode?

The podcast episode is an interview with Jacob Lund Fisker, he reached FI within 5 years by saving 85% of his income. He wrote a book and hundreds of blog posts, both called Early Retirement Extreme. By doing research for his blog he was able to make a comprehensive book outlining his strategy. The goal of the book is to present theories and principles behind Early Retirement Extreme, applicable in different contexts. Which means anyone can follow the book to get insight in a more concrete approach to the underlying philosophy. Therefore it is important to understand this philosophy, before continuing to the key takeaways.

The underlying philosophy of Early Retirement Extreme

The philosophy is outlined in the ERE manifesto. Our western society is based on consumerism, the environment is conditioned to incentivize people to spend a large part their income on stuff they don’t really need. The main goal of ERE is to do the exact opposite. Spend less than you earn, depending on how aggressively you do this it will determine when you can retire. An example of a supportive principle is that of the renaissance man. The principle is that an individual should develop a wide range of skills, to a productive level. Which will help save on labour cost, by outsourcing next to nothing and feeling more fulfilled in the process.

“Success is having everything you need and doing everything you want. It is not doing everything you need to have everything you want. If so then you do not own your things, instead your things own you.”

– Jabob Lund Fisker

The main reason I would like to recommend this episode is because it’s a proper introduction to the Early Retirment Extreme. Ofcourse it’s in the form of a interview, but like Jacob says himself: It’s not about the person but the philosophy. Since the philosophy is a complete vision on life, I would like to do further research into this topic. That is why I am currently reading the Early Retirment Extreme book, the plan is to publish my perspective when I finish the book. A link will be placed in this blog post.

What are the key takeaways?

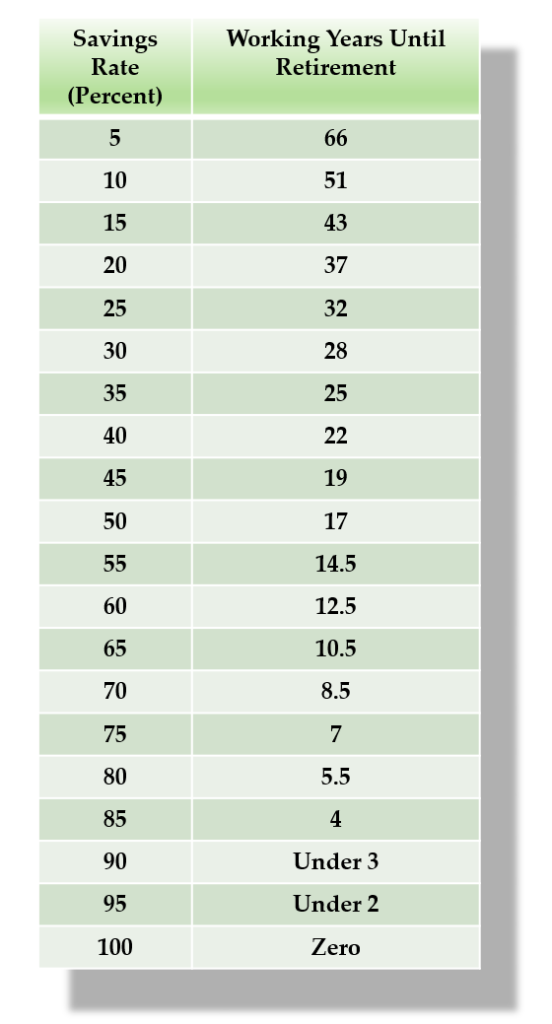

1. Your savings rate determines the early retirement date

The table on the left side illustrates the amount of time and the savings rate it requires to retire early. Starting from a zero net worth. This table is based on the following assumptions:

You get an annual 5% return on your investments, adjusted after inflation. This is doable with market returns. By example the S&P 500 index returned roughly 8% in 1957 through 2018. While by example the annual U.S. inflation in the past 20 years was only 3,1% based on the consumer price index.

You will use an annual withdrawal rate of 4% after retirment. This is a rule of thumb to withdraw while retaining the account balance.

In conclusion, the stash wil last forever. If you use the 4% rule you will only be using the gains to live off.

2. There is a problem with set and forget

As Jacob points out. There is many investors who adopt a mindset of set and forget. They setup their investment account and start to dollar cost average into ETF’s. This is a problem because paradigms shift. An example of this is the financial crisis (2008/9), which happened because debth growth rates got unsustainable. Before the crises there was the general perspective that major debt was manageable. Therefore its always important to keep an eye on trends. Pay attention, question yourself from time to time; is my investment strategy still a thing? Stay flexible with your investment strategy.

3. A systems approach to lifestyle design

The Early Retirment Extreme philosophy is based on a systems theoretic approach to lifestyle design. Which means it consists of parts, the parts are influenced by and dependend on you as a person. Also the situation you are in influences the functioning of the system. In conclusion this means that ERE allows each individual to create their own strategy to a flexible lifestyle, that is adaptable as the enviroment changes.

4. Be a renaissance man

The renaissance man is someone that has a varied range of skills on a productive level. This has multiple advantages opposed to being a specialist. You become more creative in problem solving, it allows for more possible combinations to try when solving a problem. It enables you to use your own skill-set instead of purchasing a product/service to fix the problem. Which will help you increase your savings rate. Examples of ERE skills are: Cooking, investing, gardening, carpentry.

How does it relate to Know Act Invest?

I think the Early Retirement Extreme philosophy is related to all phases of Know Act Invest. Because it is a lifestyle design approach it guides you through all the phases. From fundamentally knowing the why (Know), to formulating the how (Act) based on your situation and in the process being able to increase your savings rate accordingly (Invest). In conclusion, I hope you find this blog post informative. As mentioned earlier I am going to research this topic in further detail, to stay up to date; check out instagram.

Want to learn more about Early Retirement Extreme?

Then I recommend Jacobs Lund Fisker’s book: Early Retirement Extreme: A Philosophical and Practical Guide to Financial Independence (as an Amazon Associate I earn from qualifying purchases) The blog post focused on some key takeaways from the interview. This book is a complete guide to redesign your life, to reach financial independence. The book provides the principles and framework for a systems theoretical strategy for attaining that independence in 5-10 years. Overall I think this book is a great read, even if you adopt one aspect.

Thanks for taking an interest in this post, I would really appreciate it if you would leave a comment with feedback. This helps me to continuously improve the website.